Unveiling Concerns: Seven Reasons to Reconsider Your Investment in Nvidia, the AI Market Leader

NVIDIA-Venturebeast-Gettyimages

Introduction

Over the past thirty years, Wall Street has witnessed various investment trends capturing the imagination of investors. From the internet boom to groundbreaking innovations like genome mapping, these trends have shaped the trajectory of innovation. Currently, none is hotter than the artificial intelligence (AI) wave, a trend that has become a focal point for both investors and the financial industry.

The AI revolution involves the utilization of software and

systems to manage tasks traditionally handled by humans, with machine learning

being the game-changer. This capability allows systems to evolve and enhance

efficiency over time. With applications spanning across sectors, researchers at

PwC predict that AI could contribute up to $15.7 trillion to global GDP by

2030.

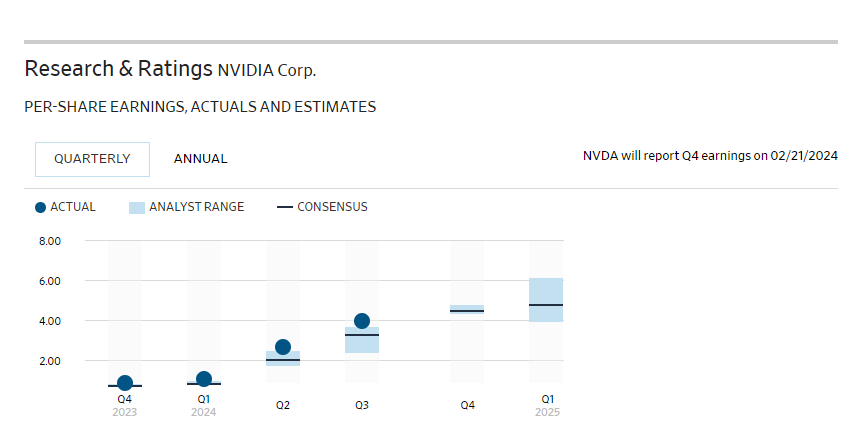

NVIDIA-preshare earning,actual and estimate

Nvidia: The Face of AI Transformation

In the realm of publicly traded companies benefiting from the AI wave, semiconductor giant Nvidia (NASDAQ: NVDA) stands out as the hottest commodity for investors. Recognized as the infrastructure backbone of the AI movement, Nvidia’s A100 and H100 graphics processing units (GPUs) facilitate split-second decisions in high-compute data centers. Citigroup analysts even suggested that Nvidia could potentially secure “at least 90%” of AI-accelerated data-center GPU share.

The company’s A100 and H100 chip production is anticipated to witness significant growth in the current calendar year, further solidifying its position in the market. Despite the jaw-dropping ascent in its stock value, increasing concerns suggest that Nvidia might not be the perpetual winner in the AI race.

Source: openai-nvidia-gpu-new-ai

Reasons to Exercise Caution

1. Nvidia Becoming its Own Obstacle

Paradoxically, the anticipated increase in output of A100 and H100 chips may adversely impact Nvidia’s gross margin. The company’s cost of revenue declined during the first half of its fiscal year 2024 due to AI-focused GPU scarcity. Now, as demand can be met more effectively, the prices of these chips are likely to fall, potentially signaling a peak in gross margin.

2. Escalating External Competition

Nvidia’s undeniable success in high-compute data centers is attracting fierce external competition. Advanced Micro Devices (NASDAQ: AMD) has introduced its MI300X AI-GPU, directly competing with Nvidia. Similarly, Intel (NASDAQ: INTC) has plans to challenge Nvidia with its Gaudi3 generative AI software chip.

3. Rising Internal Competition

In addition to external threats, Nvidia faces internal competition as some of its major clients, like Meta Platforms (NASDAQ: META) and Microsoft (NASDAQ: MSFT), develop their own AI-accelerated chips. This internal development aims to reduce dependence on Nvidia over time.

4. Regulatory Constraints

Nvidia is grappling with increasing pressure from U.S. regulators due to export restrictions on AI-driven GPUs to China. These restrictions could potentially cost Nvidia billions in potential sales each quarter.

5. Insider Selling Trends

Executives and board members at Nvidia have been consistently selling their shares for over three years, signaling potential concerns. While insiders may sell for various reasons, the absence of insider buying may raise questions about the stock’s valuation.

6. Historical Patterns

The AI movement and Nvidia face historical challenges, as previous “next-big-thing” trends have encountered early-stage bubbles, creating uncertainties about immediate market acceptance.

7. Premium Valuation in an Uncertain Industry

Nvidia’s current valuation, trading at 63X cash flow for fiscal 2024 and 90X trailing-12-month cash flow, raises eyebrows. With potential gross margin erosion and intensifying competition, Nvidia’s growth rate might face challenges.

Conclusion

While Nvidia has been the star performer in the AI realm, investors should carefully consider the emerging factors that suggest caution. The AI landscape is evolving rapidly, and uncertainties around competition, regulatory pressures, and internal challenges indicate that Nvidia’s journey might not be without hurdles. As the industry navigates uncharted territories, reevaluating the risks associated with Nvidia’s stock becomes imperative for informed investment decisions.